GAUSS Prize 2022 for Gabriela Zeller and Prof. Dr. Matthias Scherer (Research Group Finance and Actuarial Science)

Each year the German Society for Insurance and Financial Mathematics (DGVFM, e.V.) and the German Association of Actuaries (DAV, e.V.) award the prestigious GAUSS Prize and three Young Researcher Prizes for outstanding scientific work in the field of actuarial and financial mathematics.

The main prize, endowed with 3,000 euros, has been awarded for several years as the "Best Paper Award" of the European Actuarial Journal to an article published in the journal in the respective year, and for 2022 went to Gabriela Zeller and Prof. Dr. Matthias Scherer (both TUM) for their paper "A comprehensive model for cyber risk based on marked point processes and its application to insurance". The work has particularly high practical relevance, as it develops a mathematical model for cyber risk based on marked point processes, which realistically captures the dependence between cyber incidents and the resulting accumulation risk.

The prize was awarded on 22 June 2023 during the scientific symposium on the occasion of the 75th Anniversary of the DGVFM followed by a reception at KölnSKY above the roofs of Cologne.

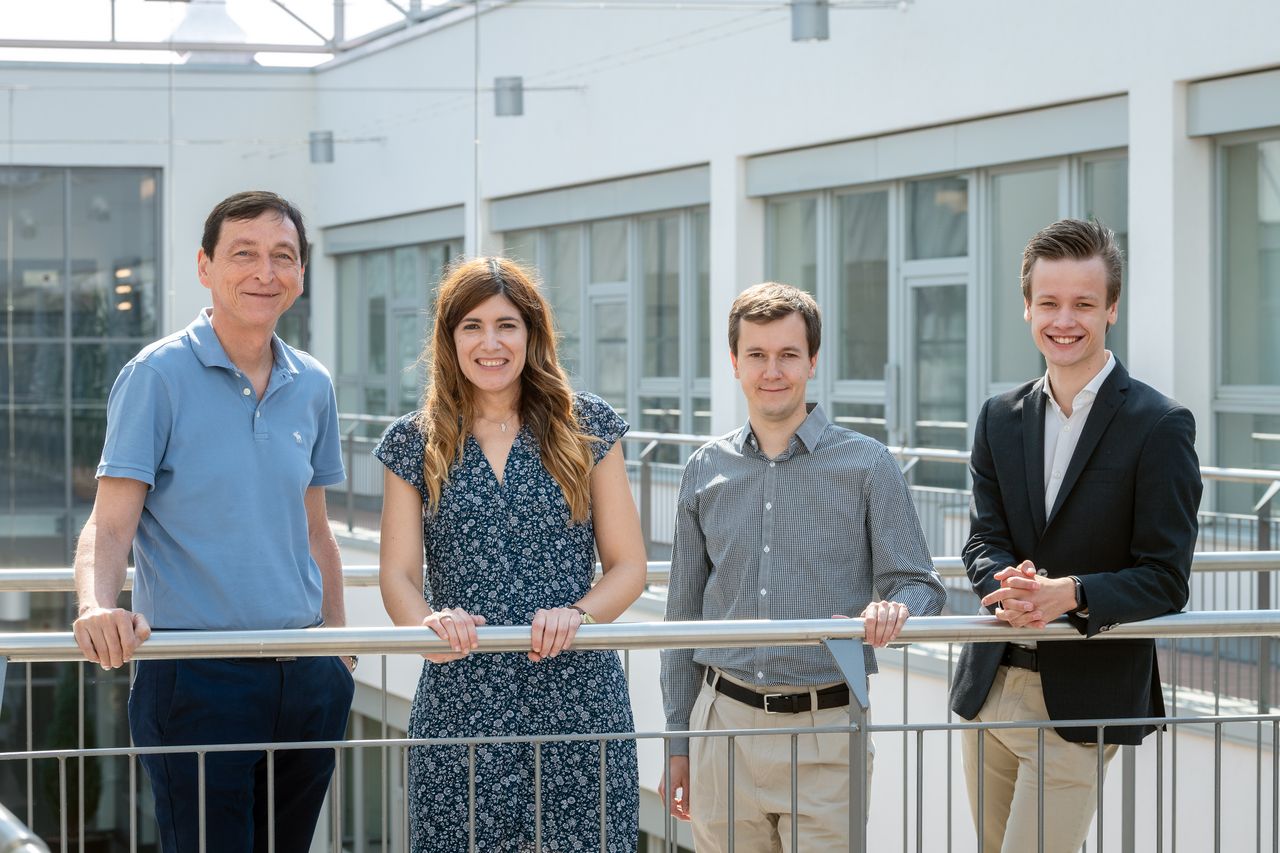

Bavarian Digital Award 2023 - former FIM students honored

Congratulations to Flora Geske (former FIM student of Prof. Dr. Rudi Zagst) and the team of SUMM AI summ-ai.com for the 1st place of the Bavarian Digital Award 2023!

Together with Vanessa Theel (also a former FIM student, on the photo on the left with Digital Minister Judith Gerlach in the middle and Flora Geske on the right) and her colleagues, Flora Geske developed an AI-supported tool that translates texts into plain language to make them more understandable for people with learning difficulties, for example.

Best presentation award at the 11th Conference in Actuarial Science and Finance in Samos

The Conference in Actuarial Science and Finance takes place every two years as part of a joint collaboration between the University of the Aegean, Katholieke Universiteit Leuven, Kobenhavns Universitet and New York University. It is a forum for state-of-the-art results in the areas of insurance, finance and risk management, and attracts top academicians and practitioners from every corner of the world.

The scientific committee of the 11th Edition of the conference, held in Karlovasi (island of Samos, Greece) awarded Gabriela A. Zeller, PhD candidate at Chair of Mathematical Finance of the Technical University of Munich, with the 1st prize of the Best Presentation Awards for young researchers. Her joint work with Prof. Matthias Scherer (TUM) titled “Optimal price structure of cyber insurance policies with risk mitigation services” analyses under which conditions it can be profitable for an insurance company to subsidize pre- and post-incident services within cyber insurance policies.

Teaching Award Golden Circle in Summer Semester 2021

In the winter semester 2021/22 the mathematics department awards teaching prizes for outstanding teaching in the past semester.

Our chair can be pleased about two awards in the category "Best Advanced Lecture":

2nd place: Portfolio Analysis (MA4706) by Prof. Dr. Rudi Zagst and Henrik Sloot.

3d place: Insurance Mathematics 2 (MA3406) by Prof. Dr. Matthias Scherer and Dr. Markus Wahl

SCOR Prize Actuarial Science 2021

Every year since 1996, SCOR has awarded the best academic papers in the field of actuarial science with annual prizes in several countries around the world. These awards aim to promote the development of actuarial science, stimulate research in the field and contribute to the improvement of risk knowledge and management. The SCOR Actuarial Awards are recognized as a mark of excellence in the insurance and reinsurance industry. The SCOR Actuarial Awards juries are composed of internationally recognized researchers and insurance, reinsurance and finance professionals. Winners are selected based on their mastery of actuarial concepts, the quality of their analytical methods and the originality of their research in terms of scientific advances and potential practical applications in the world of risk management. In 2021, SCOR presented actuarial awards in five countries around the world: Germany, France, Italy, Sweden and Switzerland. In Germany, Maria Hinken from the Technical University of Munich was one of two winners of the SCOR Actuarial Award for her thesis "Life insurance products with capital guarantees : Stackelberg equilibria between reinsurer and insurer".

Ms. Hinken's master's thesis was supervised by Prof. Dr. Rudi Zagst (Chair) and Yevhen Havrylenko (PhD student) at the ERGO Center of Excellence in Insurance and appears as part of the third edition of the "ERGO Master Series".

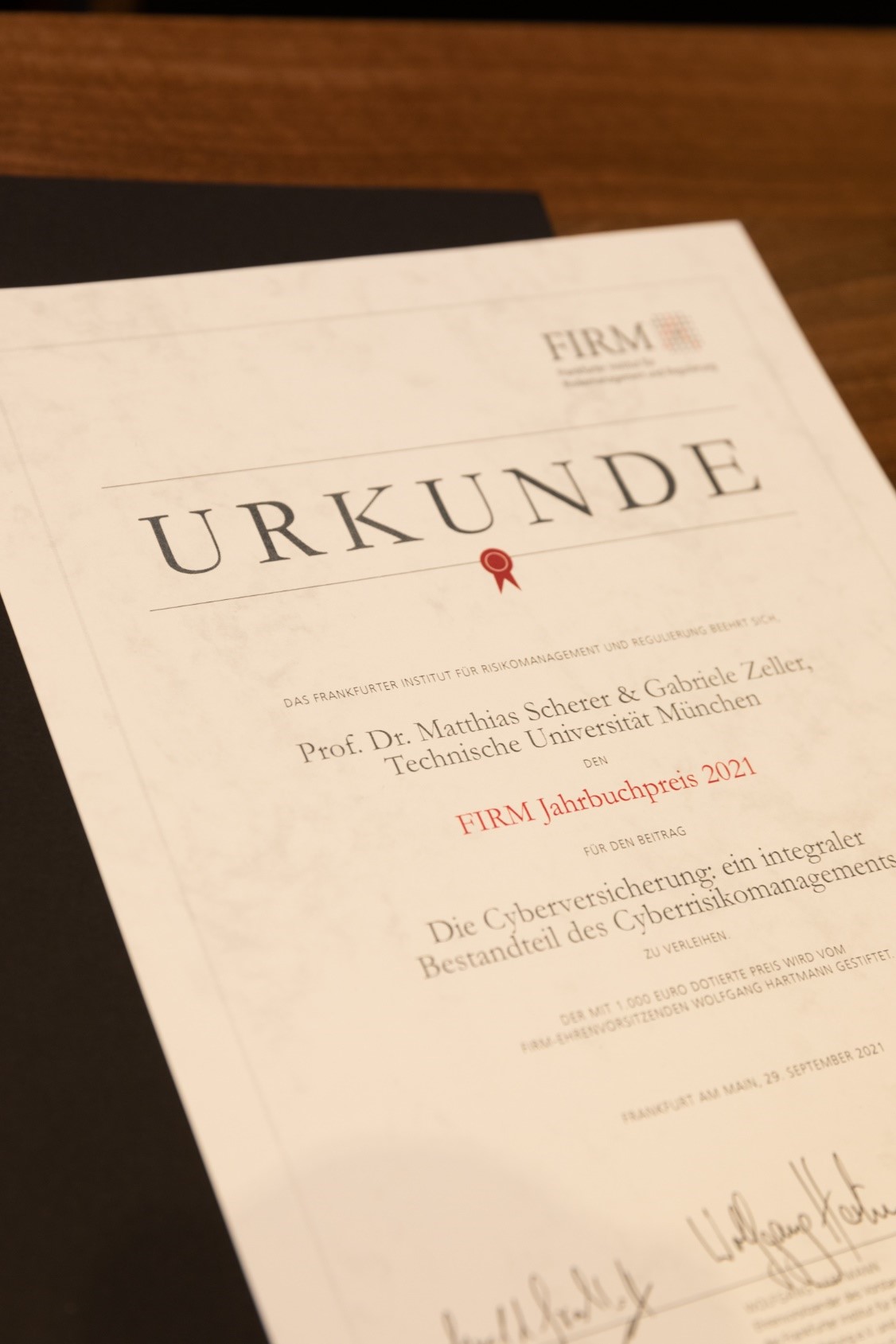

Article on Cyber Insurance awarded FIRM Yearbook Award 2021

As every year, the Frankfurt Institute for Risk Management and Regulation (FIRM, e.V.) has published a yearbook with numerous invited expert contributions (accessible here: https://www.firm.fm/).

The article contributed by Gabriela Zeller and Prof. Dr. Matthias Scherer (both at the Chair of Mathematical Finance) on the topic “Cyber Insurance: An integral component of Cyber Risk Management” has been awarded the Yearbook Award 2021 by a commission of experts from academia and industry.

The article surveys today’s cyber insurance market in terms of products and types of coverage and explains which factors determine a company’s risk category and, hence, insurance premium. Furthermore, it describes limits of insurability of cyber risk and highlights the influence of `silent cyber’ on traditional insurance policies.

The prize was officially awarded during the hybrid annual FIRM event in autumn 2021.

Master's thesis at ERGO Center of Excellence awarded 2nd SCOR Actuarial Science Prize 2020

The master thesis "Customer Churn Prediction In The Insurance Sector Using Machine Learning Methods" written by Ms. Bassant Abed was awarded a 2nd prize in the competition for the German SCOR Prizes for Actuarial Science 2020.

Every year, SCOR in Germany awards prestigious prizes for outstanding work to promote the next generation of actuarial scientists. In cooperation with the University of Ulm, the prizes are awarded to papers dealing with relevant actuarial topics in personal and property insurance. Due to special circumstances, the 2020 award ceremony took place virtually (https://www.scor.com/en/press-release/scor-supports-actuarial-science-presenting-actuarial-awards-five-countries-2020).

As part of her thesis, Ms. Abed addresses the further development of traditional lapse prediction models using machine learning methods to combine high predictive power and potentially improved interpretability. In a case study, a large real-world dataset is suitably pre-processed before several classes of predictive models are implemented and compared using appropriate performance metrics. In addition, insight into applicable measures and interpretability methods is provided so that insurers can take effective lapse reduction actions based on the modeling. Thus, the presented models can contribute to customer retention by identifying relevant lapse drivers in a timely manner and then applying the proposed measures to prevent customer churn.

Ms. Abed's paper was supervised by Prof. Dr. Matthias Scherer (Professor for Risk and Insurance) and Gabriela Zeller at the ERGO Center of Excellence and appears as part of the second edition of the "ERGO Master Series". Special thanks are also due to the practice experts at ERGO Group AG, who supported Ms. Abed's work by providing an extensive real-world data set.

TopMath Study Award for Ben Spies

Ben Spies, a doctoral student in the Department of Financial Mathematics and supervised by Professor Rudi Zagst, was awarded the TopMath Study Award at the conclusion of the elite master's program in the TopMath program. The award, endowed with 500 euros, was presented to Ben Spies for outstanding performance in the modules of the program, where current results of his joint research with Professor Zagst and Professor Marcos Escobar-Anel were also incorporated via the lectures in the Independent Studies and via the master's thesis.

Good Teaching Award of the Mathematics Student Council

Based on the teaching evaluations, the student council of the mathematics department has awarded Prof. Zagst and Dr. Wahl for the advanced lecture Applied Risk Management, Dr. Fernandez for the tutorial on Insurance Mathematics and Mr. Kschonnek for the tutorial on Fixed Income Markets for particularly successful teaching in the winter semester 2020/21. Congratulations!

Andreas Lichtenstern receives GAUSS Young Investigator Award for outstanding doctoral thesis

The German Society of Actuaries and Financial Mathematicians (DGVFM) and the German Actuarial Association (DAV) awarded the prestigious GAUSS Prize and three GAUSS Young Investigator Prizes for outstanding scientific work in the field of actuarial and financial mathematics on June 8, 2021. With the awards, the high-ranking expert committee from science and practice selects technical papers that bridge the gap between scientific quality and high practical relevance.

Andreas Lichtenstern was awarded the GAUSS Young Investigator Award for his dissertation "Optimal Investment Strategies for Pension Funds." "The particular innovation of this work lies in the fact that it solves previously open mathematical problems concerning optimal investment strategies for pension funds and applies them to the social partner model that has become known as the Nahles pension," said Prof. Müller in praise of the doctoral thesis.

Good Teaching Award of the Mathematics Student Council

Based on the teaching evaluations, the student council of the mathematics department has awarded Prof. Dr Rudi Zagst, PD Dr Aleksey Min and Dr Lexuri Fernandez for their very good teaching in the winter semester 2019/20 with prizes for their great commitment in teaching. Congratulations!

10.07.2020

Teaching Award for Prof. Dr. Peter Hieber

During the graduation ceremony on 12.07.2019, Prof. Peter Hieber was awarded for the conception of the lecture "Actuarial Risk Management" (WiSe 2018/19). He received one of the teaching awards "Goldener Zirkel" of the mathematics student council (category: practice). We sincerely thank the students for this very nice award.

14.08.2019

Big honour for the Chair of Mathematical Finance at the graduation ceremony WiSe 2017/18

- Slide 1(Current Item)

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

An astonishing four Awards were handed to the chair of mathematical Finance at the recent graduation ceremony. Prof. Dr. Rudi Zagst was awarded first place for the best advanced lecture "Investment Strategies". Prof. Dr. Matthias Scherer has accomplished second place in the "ISAM Supervisory Awards 2018". Dr. Lexuri Fernandez achieved first place for the best tutorial "Investment Strategies" while PD Dr. Aleksey Min achieved second place for his "Fixed Income Markets" tutorial. Congratulations to the recipients for this huge success and the confirmation of their excellent work.

16.07.2018

Second place for Prof. Rudi Zagst

Professor Zagst is happy to be awarded the second place for his postgraduate lecutre. Each semester, this prize is awarded for the best basic- and postgraduate lecture. Professor Zagst was awarded for the lecture "Portfolio Analysis" of the sommer semester 2017.

21.02.2018

Teaching Prize "Goldener Zirkel" and more

Dr. Daniel Linders (Fixed Income Markets) is happy to be awarded the teaching prize "Goldener Zirkel" by the student council of mathematics. The prize was awarded for the "Best Tutorials" of the winter semester 2016/17. Dr. Lexuri Fernandez as well as Amelie Hüttner (both: Financial Engineering with Copulas) were honored with the third place in this category. We expresse our deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

08.07.2017

Prof. Scherer awarded Teaching Prize "Goldener Zirkel" and Prof. Zagst the third place

Professor Scherer is happy to be awarded the teaching prize "Goldener Zirkel" by the student council of mathematics. Each semester, this prize is awarded for the best basic- and postgraduate lecture. In the category 'postgraduate lecture', the prize was awarded for the lecture "Financial Engineering with Copulas" of the winter semester 2016/17. Professor Zagst was awarded the third place for his lecture "Fixed Income Markets" in same category. Professor Scherer and Professor Zagst expresse their deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

08.07.2017

Second place for Prof. Rudi Zagst

Professor Zagst is happy to be awarded the second place for his postgraduate lecutre. Each semester, this prize is awarded for the best basic- and postgraduate lecture. Professor Zagst was awarded for the lecture "Portfolio Analysis" of the sommer semester 2016.

21.12.2016

SCOR Preis 2016 for Daniela Selch

Daniela Selch did her dissertation at the chair of Mathematical Finance at TUM. Her dissertation "A multivariate Cox process with simultaneous jump arrivals and its application in insurance modelling" was supervised by Prof. Matthias Scherer. Daniela was awarded the SCOR Preis 2016 for her dissertation.

19.12.2016

Excellence Award 2016 for Dr. Steffen Schenk

Dr. Steffen Schenk was awarded the Excellence Award for his dissertation „Exchangeable exogenous shock models“ (supervised by Prof. Dr. Matthias Scherer) on the September 29th 2016 in Hamburg. The thesis deals with modeling high dimensional random vectors and applying shock models in order to evaluate and to manage credit or insurance portfolios.

The Excellence Award is annually awarded by the Verein zur Förderung der Versicherungswissenschaft in Hamburg (VFVH) and is endowed with 1500 €. Its aim is to promote and motivate young researchers in the field of Financial/ Insurance Mathematics to deal with unsolved questions in the field of Actuarial Science.

05.10.2016

Post Bank Finance Award 2016

Gabriela Galic, Daniel Kehne, Christian Olenberger, Maximilian Siegert, Andreas Sperling and Florian Zyprians, all FIM students, as well as their superviser Dr. Markus Böhm of TU Munich were able to achieve the 1st place of the Postbank Finance Award, which is endowded with 50.000 €.

Their topic "FinTechs lieben lernen" analysis first the value streams of banks and FinTechs and gives then strategy advices for banks. Congratulations!

04.07.2016

Prof. Zagst receives "Golden Circle" teaching award

Professor Zagst is happy to be awarded the third place of teaching prize "Goldener Zirkel" by the student council of mathematics. In the category 'postgraduate lecture', the prize was awarded for the lecture "Portfolio Analysis" of the summer term 2013. Professor Zagst expresses his deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

16.01.2014

PD Min awarded Teaching Prize "Goldener Zirkel"

PD Aleksey Min is happy to be awarded the teaching prize "Goldener Zirkel" by the student council of mathematics. The prize was awarded for the "Best Tutorials" of the winter semester 2015/16. PD Aleksey Min expresses his deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

01.07.2016

GAUSS-Prize 2015 for young researchers awarded to Dr. Steffen Schenk

Dr. Steffen Schenk was awarded the GAUSS-prize for young researchers for his dissertation „Exchangeable exogenous shock models“ (supervised by Prof. Dr. Matthias Scherer).The thesis deals with modeling high dimensional random vectors and applying shock models in order to evaluate and to manage credit or insurance portfolios.

The GAUSS-Prize is awarded annually by the German Society of Financial/Insurance Mathematics (DGVFM) and the German Actuarial Association (DAV) and is endowed with EUR 2.000. Its aim is to promote and motivate young researchers in the field of Financial/ Insurance Mathematics to deal with unsolved questions in the field of Actuarial Science. Specifically desired are contributions that bridge the gap between scientific quality and practical relevance. The GAUSS-Prize 2013 was awarded on April 29th 2016 at the Scientific Day of DAV/DGVFM in Bremen.

09.05.2016

Double Success at MINT-Award 2014!

Within the framework of the official ceremony of the "MINT-Award Mathematik 2014", which took place October 17th 2014, two outstanding theses of the chair of Mathematical Finance have been awarded a prize according to the motto "Model:= Truth?! Strengths and Weaknesses of models within actuarial mathematics". Sebastian Walter has been awarded with the first place and prize money amounting to 300 € for his Master's Thesis on "Credit Valuation Adjustments and Wrong-Way Risk - A Comprehensive Case Study of Counterparty Default Risk". The thesis has been supervised by Prof. Dr. Matthias Scherer of the Chair of Mathematical Finance and Dr. Stephan Höcht from Assenagon Asset Management S.A. The third place, accompanied by prize money amounting to 500 €, has been awarded to Oskar Gruber, for his Bachelor's thesis on "Value at Risk forecasting and backtesting with the ARMA-GARCH family", which has been praised as especially innovative by the jury. The thesis has been supervised by Dr. Georg Mainik from the ETH Zurich, who had a visiting professorship during the summerterm in 2014 at the Chair of Mathematical Finance.

22.10.2014

"The Supermartingales" achieve 1st place along with over 25.000 € prize money at stock exchange competition

Within the scope of the trading competition among universities across Europe, which has been organized for the 4th time by Italian online broker "Directa", Mirco Mahlstedt, Steffen Schenk and Thorsten Schulz were able to achieve 1st place with their team „The Supermartingales“. Beside the trading surplus of 6.048,73 € they obtained and get to keep to themselves, the Chair of Mathematical Finance, on whose behalf the Supermartingales competed, gets 20.000 € prize money, which is available for teaching and research purposes.

Each of the 111 university teams from 12 different countries had been equipped with an initial amount of 5.000 € by Directa. The goal was to achieve the highest possible return within one year, without falling below the threshold of 3.000 €. Beside company shares and bonds, teams were also able to trade commodities, foreign exchange as well as volatility derivatives.

By the end of the trading period, the Supermartingales had achieved a total gain of 120,97 %, which corresponds to a deposit value of 11.048,73 €. With this result they were able to secure a clear lead over their competition. The prize ceremony took place on May 23rd 2014 within the scope of the Investment & Trading Forum in Rimini, Italy's biggest investor fair.

16.07.2014

GAUSS-Prize for young researchers awarded to Peter Hieber

Dr. Peter Hieber was awarded the GAUSS-prize for young researchers for his dissertation „First-exit times and their applications in default risk management“ (supervised by Prof. Dr. Matthias Scherer). The thesis deals with modeling and managing default risk in Finance and Insurance.

The GAUSS-Prize is awarded annually by the German Society of Financial/Insurance Mathematics (DGVFM) and the German Actuarial Association (DAV) and is endowed with EUR 2.000. Its aim is to promote and motivate young researchers in the field of Financial/ Insurance Mathematics to deal with unsolved questions in the field of Actuarial Science. Specifically desired are contributions that bridge the gap between scientific quality and practical relevance. The GAUSS-Prize 2013 was awarded on April 30th 2014 at the Scientific Day of DAV/DGVFM in Bonn.

21.05.2014

Prof. Zagst awarded Teaching Prize "Goldener Zirkel"

Professor Zagst is happy to be awarded the third place of teaching prize "Goldener Zirkel" by the student council of mathematics. In the category 'postgraduate lecture', the prize was awarded for the lecture "Portfolio Analysis" of the summer term 2013. Professor Zagst expresses his deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

16.01.2014

Prof. Dr. Zagst and Mikhail Krayzler received GAUSS-Preis 2012

The GAUSS-Prize is awarded annually by the German Society of Financial/Insurance Mathematics (DGVFM) and the German Actuarial Association (DAV) and is endowed with EUR 15.000. Its aim is to promote and motivate young researchers in the field of Financial/ Insurance Mathematics to deal with unsolved questions in the field of Actuarial Science. Specifically desired are contributions that bridge the gap between scientific quality and practical relevance. The GAUSS-Prize 2012 was awarded at the Scientific Day (24.-26. April 2013) of DAV/DGVFM. Prof. Dr. Rudi Zagst and Mikhail Krayzler were awarded for their contribution "Closed-form solutions for Guaranteed Minimum Accumulation Benefits".

28.05.2013

Assenagon Thesis Award in Finance 2012

For the third time in a row this year’s Assenagon Thesis Award in Finance was conferred by the Chair of Financial Mathematics of TU Munich within the framework of the FitForTUMorrow Day on 23 November 2012. The prize honors outstanding final theses in the area of Financial Mathematics which were submitted either at TU Chemnitz, the University of Duisburg-Essen, TU Kaiserslautern, the Karlsruhe Institute of Technology or TU Munich. The prize was founded by Vassilios Pappas, a co-founder of Assenagon, and Prof. Dr. Matthias Scherer of the Chair of Financial Mathematics of TU Munich.

In his lecture Michael Hünseler (Managing Director of Assenagon Asset Management S.A.) pointed out the wide range of distinguished papers and expressed his thanks to the participating professors Nicole Bäuerle (Karlsruhe Institute of Technology), Rüdiger Kiesel (University Duisburg-Essen), Ralf Korn (TU Kaiserslautern), Thorsten Schmidt (TU Chemnitz), Matthias Scherer and Rudi Zagst (both TU Munich). Subsequently the laureates of the universities shortly presented their papers.

In the absence of Derya Baghistani (University Duisburg-Essen), Michael Kustermann (tutor of the paper and first Assenagon Thesis Award Overall Winner 2010) presented her paper about "Assessment of a power plant in a hybrid stochastic model”. He was followed by Rick Hofmann (TU Chemnitz) who lectured about "Statistical analysis of electricity models“. Thereupon Anton Popp (Karlsruhe Institute of Technology) presented his paper about "Portfolio Optimization using SAHARA utility functions”. Nina Sörgel (TU Munich) explained her analysis of "Variance reduction schemes for Monte Carlo methods in portfolio credit risk". Finally Songyin Tang (TU Kaiserslautern) presented his paper about "SABR Model in Interest-Rate World and Correction of Labordere's Option Pricing Formula in the Normal SABR Case".

Dr. Stephan Höcht and Patrick Spitaler appreciated the high quality of the submitted papers and awarded the individual university winners. Songyin Tang was selected as the overall winner of the Assenagon Thesis Award in Finance 2012.

15.12.2012

SCOR Preis 2012 (3. Platz) for Daniel Geldner

Daniel Geldner was awarded for his master thesis „Weather Derivatives and Electricity Demand Modeling“, supervised by Prof. Matthias Scherer, PD Alexey Min and Ralf Hungerbühler (Munich Re). The jury praised the unusal and very intersting topic of the electricity demand's simulation depending on temperature and applicability in the business practice. The official award ceremony took place on 19 November 2012 in Worpswede near Bremen.

26.11.2012

Prof. Scherer Awarded Teaching Prize "Goldener Zirkel" for his Lecture "Credit Derivatives"

For the second time already, Professor Scherer is happy to be awarded the teaching prize "Goldener Zirkel" by the student council of mathematics. Each semester, this prize is awarded for the best basic- and postgraduate lecture. In the category 'postgraduate lecture', the prize was awarded for the lecture "Credit Derivatives" of the winter semester 2011/12, which German Bernhart was significantly involved in as a tutor. Professor Scherer expresses his deepest thanks to the students for this great honouring and the always pleasant working atmosphere.

29.06.2012

FIM Students Awarded Postbank Finance Award

On June 22, 2012, the team of students of TU München ranked 3rd at the Postbank Finance Award. Within the framework of this competition and together with Prof. Dr. Rudi Zagst, the students Michael Ludwig, Mirco Mahlstedt and Herbert Mayer analysed "Inflation-Protected Investment Strategies". The prize is endowed with prize money of 15,000 EUR, which is for the benefit of the chair as well as the team.

Prize winner Mirco Mahlstedt says about their contribution to this competition: "We have analysed what a portfolio of shares, state bonds, real estates and raw materials should be made of in different scenarios and market situations in order to be protected against inflation. First, we have dealt with the question if inflation periods can be made out and forecasted at an early stage whereupon we have developed a dynamic investment strategy. It was advantageous for us that we had already dealt with this topic within the framework of our Bachelor theses and that we intended to analyse it in detail within the framework of our Master study in the field of financial- and information management anyway. This is the reason why the subject of financial investment at inflation- and political risks of this competition of Postbank was perfect for us."

Since 2003, the Postbank Finance Award is offered every year. It aims at finding innovative and scientifically substantiated answers to current financial questions according to the motto "Understand the Future - Create the Future". By means of this prize, the bank does not only aim at encouraging students of all fields of study to deal with any relevant question in business finance but offers the participating students help and presents ideas to them for their future studies and career planning. 70 percent of the prize money is used to equip the awarded universities.

22.06.2012

GAUSS Prize 2011 Awarded to K. F. Bannör and M. Scherer

Karl Friedrich Bannör and Prof. Dr. Matthias Scherer are awarded the 2nd GAUSS Price 2011 for their publication "Quantifying the degree of parameter uncertainty in complex stochastic models". In his laudatory speech, Prof. Dr. Ralf Korn particularly praises that the publication is innovative and of practical relevance for allowing parameter risk for the price of exotic derivatives and for comparing the parameter risk of models.

Every year, the GAUSS Prize is offered by the Deutsche Gesellschaft für Versicherungs- und Finanzmathematik (DGVFM) (German Association for Actuarial and Financial Mathematics) in cooperation with the Deutsche Aktuarvereinigung (DAV) (German Actuarial Association). It is awarded for cutting-edge publications of practical relevance in which problems and topics of actuarial science are detected and tackled appropriately. The prize is to support and motivate young actuaries as well as actuarial- and financial mathematicians in studying open questions and tasks of actuarial science.

The GAUSS Prize 2011 has been awarded on the Scientific Day within the framework of the annual convention of DAV and DGVFM in Stuttgart from April 25 through 27, 2012. It is endowed with prize money of 15,000 EUR and has been awarded for the eleventh time already.

09.05.2012

2nd Assenagon Thesis Award Goes to Ludwig Schmid (TUM)

Within the framework of the FitForTUMorrow Day of the faculty of financial mathematics on December 2, 2011, the Assenagon Thesis Award in Finance has been awarded for the second time already. The prize honours final theses in the field of financial mathematics, which have been submitted to the University of Duisburg-Essen, TU Kaiserslautern, Karlsruhe Institute for Technology and TU Munich. The prize had been launched by Vassilios Pappas, one of the founders of Assenagon, and Prof. Dr. Matthias Scherer from the faculty of financial mathematics of TU Munich.

Prof. Dr. Rudi Zagst and Dr. Wolfgang Klopfer (CEO, Assenagon Credit Management GmbH) gave the inaugural address, in which they both pointed out what the award aims at, namely to promote research in the field of financial mathematics. Their speech was followed by a short presentation of the universities' prize winners about their theses. Alona Futorna (TU Kaiserslautern) presented her thesis about "Universal Binomial Trees for Option Pricing" followed by Tobias Hufschmidt (University of Duisburg-Essen) who spoke about "Optimised Power Procurement in Energy-Intensive Industry". Maximilian Scheffler (Karlsruhe Institute for Technology) presented his thesis "Self-Energising Effects in Intensity Models of Credit Risk" and at last Ludwig Schmid spoke about "A new portfolio credit default model based on a CIID construction with shot-noise processes" .

Dr. Stephan Höcht and Dr. Jan Mai praised the high quality of the submitted theses and awarded the individual prize winners. Ludwig Schmid was awarded overall winner of the Assenagon Thesis Award in Finance 2011.

02.12.2011

Actuary Prize 2011 of SCOR Awarded to Helmut Artinger

For his diploma thesis Longevity Risk in the Pension Context, Helmut Artinger is awarded the actuary prize of SCOR. On November 15, 2011, the prize was handed over by Frieder Knüpling, Deputy CEO of SCOR Global Life, in the presence of Michel Dacorogna, Deputy Chief Risk Officer of SCOR.

15.11.2011

Scholarship for Young Academics of DGVFM Awarded to Steffen Schenk

Steffen Schenk, Finance and Information Management student at TUM (Technical University of Munich) and the University of Augsburg, was awarded the Scholarship for Young Academics of DGVFM. By means of this scholarship he gets the chance to translate his diploma thesis into an article ready to be published and have it released in a trade journal. For this, he is granted a time period of six months. In his master thesis, he analyses a multivariate default model, the application of which in credit risk modelling is analytically and empirically analysed. His thesis was supervised by Dr. Jan-Frederik Mai (Assénagon Credit Management), Prof. Pablo Olivares and Prof. Matthias Scherer.

30.09.2011

Scholarship of the Deutsche Gesellschaft für Versicherungs- und Finanzmathematik (DGVFM) e.V. Awarded to Helmut Artinger

Mr. Helmut Artinger, mathematics student at TUM (Technical University of Munich), is awarded the Scholarship for Young Academics of DGVFM (German Association for Actuarial and Financial Mathematics). By means of this scholarship he gets the chance to translate his diploma thesis into an article ready to be published and have it released in a trade journal. For this, he is granted a time period of six months. The diploma thesis is supervised by c and the business partner risklab and is about Longevity Risk in the Pension Context.

07.07.2011

GAUSS Prize 2010 Awarded to A. Schlösser and R. Zagst

Dr. Anna Schlösser and Prof. Rudi Zagst are awarded the 1st GAUSS Prize 2010 for their publication The Crash-NIG copula model: modeling dependence in credit portfolios through the crisis. In his laudatory speech, Prof. Dr. Dietmar Pfeifer particularly praises that the publication is of topical relevance.

Dr. Jan-Frederik Mai is awarded the Young Academics Prize for his dissertation Extendibility of Marshall-Olkin distributions via Lévy subordinators and an application to portfolio credit risk.

Every year, the GAUSS Prize is offered by the Deutsche Gesellschaft für Versicherungs- und Finanzmathematik (DGVFM) (German Association for Actuarial and Financial Mathematics) in cooperation with the Deutsche Aktuarvereinigung (DAV) (German Actuarial Association). It is awarded for cutting-edge publications of practical relevance in which problems and topics of actuarial science are detected and tackled appropriately. The prize is to support and motivate particularly young actuaries as well as actuarial- and financial mathematicians in studying open questions and tasks of actuarial science.

The GAUSS Prize 2010 has been awarded on the Scientific Day within the framework of the annual convention of DAV and DGVFM in Stuttgart from April 27 through 29, 2011. It is endowed with prize money of 15,000 EUR and has been awarded for the tenth time already.

07.07.2011

Prize of Deutsches Aktieninstitut (DAI) Awarded to Peter Hieber

Within the framework of the annual press conference of DAI (German Institute for Alternative Investments), Peter Hieber was awarded the 1st prize in the category of diploma-/master thesis. In the assessment, DAI mainly considered the overall impression of the thesis, its innovation and originality as well as if the problem it deals with and solves is relevant for the work of DAI. Peter Hieber wrote his diploma thesis about Incorporating Default Risk in an Equity Portfolio Optimization in cooperation with the University of Toronto / Ryerson University Toronto. The thesis was supervised by Prof. Matthias Scherer (HVB Institute for Mathematical Finance) and Prof. Marcos Escobar (Toronto).

13.04.2011

BAI Science Award (Bundesverband Alternative Investments e.V.) in the Field of Diploma Theses Awarded to Theresa Krimm for her Master Thesis "Asset Allocation and Sustainability in Turbulent Market Phases"

BAI SCIENCE AWARD: For the first time ever, the Bundesverband Alternative Investments e.V. (German Federal Association of Alternative Investments) has awarded the BAI Science Award in the field of alternative investments for excellent scientific work this year. Theses of four different categories were awarded. The awards are endowed with prize money of all in all EUR 10.000. In the category of Master thesis, the jury of six members from science and industry awarded the prize to Theresa Krimm for her thesis about "Asset Allocation and Sustainability in Turbulent Market Phases", which she wrote one year before within the programme of Finance & Information Management and which was supervised by Prof. Dr. Rudi Zagst.

14.02.2011

Student Council of Mathematics Awards Teaching Prize to Prof. Scherer

On November 26, 2010, Prof. Matthias Scherer is awarded a special prize: Within the framework of the farewell celebrations for the graduates in mathematics at TUM, the student council of mathematics awards Professor Scherer the prize for the best advanced lecture (Continuous Time Finance, MA 3702). This prize has been awarded for the first time ever.

Prof. Scherer said about the prize: "I would like to express my deepest thanks to all people who attended the lecture for the always pleasant working atmosphere and their many constructive questions and feedback. Finally it is the students themselves who mostly decide upon a lecture's success. Let me also take this opportunity to thank Dr. Jan-Frederik Mai for having contributed a lot to this success by his excellent exercises and the trainers of ProLehre for their brilliant teaching advice."

26.10.2010

assénagon Thesis Award Goes to Peter Hieber

On the occasion of the FitForTUMorrow Day on November 25, 2010, Peter Hieber is conferred the assénagon Thesis Award in Finance for his diploma thesis Incorporating Default Risk in an Equity Portfolio Optimization.

25.11.2010

Double Victory in DZ Bank Career Prize 2010

FIM students attended by Prof. Dr. Rudi Zagst came out on top of the DZ Bank Career Prize 2010! Cornelia Ernst is awarded the first prize for her Master thesis about Weaknesses of "Value at Risk". The students German Bernhart, Michael Neugebauer and Michael Neumann are awarded the first prize, too, in the respective category for their Bachelor thesis about "Asset Correlations in Turbulent Markets".

14.10.2010

DZ Bank Career Prize 2009 for FIM Students

The FIM students Darius Abde-Yazdani, Sven Hroß, Theresa Krimm, Johannes Rauch, Sebastian Stamm and Christofer Vogt are awarded the DZ Bank Career Prize 2009 for their thesis "In Pursuit of a Sustainable World: Socially Responsible Investing and Eco Investments".

12.11.2009

DZ Bank Career Prize 2008 for FIM Students

The FIM students Philipp Aigner, Georg Beyschlag, Tim Friederich and Markus Kalepky are awarded the DZ Bank Career Prize 2008 for their thesis "Private Equity as an Asset Class".

28.10.2008

Jan-Frederik Mai Awarded Sponsorship Prize

Jan-Frederik Mai is awarded the sponsorship prize of the "Ulmer Forum für Wirtschaftswissenschaften" (Ulm Forum of Economic Sciences) and SÜDWEST PRESSE.

17.07.2008

Matthias Scherer awarded Südwestmetall Prize

Dr. Matthias Scherer is awarded the "Südwestmetall Prize for Young Academics 2007" of the trade association of metal and electrical industry. Scherer's "incredibly brilliant scientific career so far" is particularly praised in the laudatory speech.

28.11.2007

Rudi Zagst 'Professor of the Year'

The magazine UNICUM BERUF elects Prof. Dr. Rudi Zagst "Professor of the Year 2007". In cooperation with the auditing and consulting firm KPMG, UNICUM BERUF surveyed students, graduates, professors and employers which professors support their students' careers most. Zagst is conferred the title in the category of natural sciences and medical science.

29.09.2007